by Olevia Sharbaugh Starkey, Economist at Dodge Construction Network

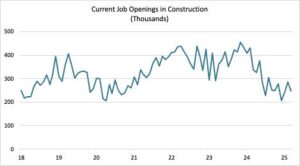

After two months of strong growth, construction job openings in March experienced a greater decline than total U.S. openings. While construction job openings declined 13% to 248,000, the Bureau of Labor Statistics’ estimate of total U.S. job openings came in only 4% lower than the revised February estimate at 7.2 million in the latest #JOLTS report. Both hires (-13%) and total separations (-10%) in the construction industry declined by double digits in March, also much weaker than the +1% in hires and -3% in total separations the total U.S. labor market experienced. While much of this points to outsized weakness in the construction industry, it is important to note that this data series fluctuates much more than the overall U.S. dataset, and the pre-pandemic averages (2010-2019) for openings, hires, and total separations for the construction industry remain close to current year-to-date estimates.

Although the U.S. labor market has been moderating from the post-pandemic highs for some time now, this more recent weakness is likely due to macroeconomic uncertainty created by the ever-shifting tariff policies. Without clearly defined and stable economic policy to count on, companies are more likely to delay staffing decisions until they have more clarity. Though it may be too early to tell, it appears that construction firms are being more cautious than those in other industries when it comes to their labor decisions. Given that both the tariff and immigration policies will have outsized impacts on the sector, this isn’t an unexpected effect. For example, the current effective tariff rate on U.S. imports is approximately 25–30%, but the effective rate on construction goods is a few percentage points higher due to the industry’s product mix and the countries from which these products are sourced. The change in the U.S. effective tariff rate indicates that overall inflation will increase 2%–3% over the next year, but construction costs will rise around 0.5 to 0.75 ppt higher due again to the input product mix.

While the risks to the construction industry remain high, it will take more time to accurately assess the impact these policies will have on the future of the industry.

Make sure to keep following along to see how this will affect construction starts in the future.

Data Source: https://www.bls.gov/jlt/