According to the U.S. Bureau of Labor Statistics’ latest release of the Producer Price Index (PPI) for June, the PPI for final demand experienced a modest increase of 0.1%, after a decline of 0.4% in May. This upturn can be primarily attributed to a consistent 0.2% increase in the index for final demand services, mirroring the previous month’s trend, while prices for final demand goods remained steady. Over the 12-month period ending in June, the unadjusted index for final demand showed a modest advancement of 0.1%.

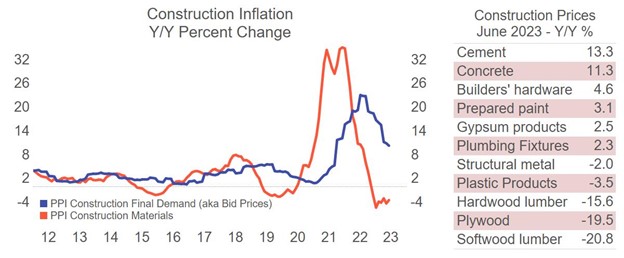

In June, the index for final demand less foods, energy, and trade services saw a 0.1% increase, signaling a steady upward trend following no change in May. However, it’s important to note that the index for final demand transportation and warehousing services experienced a decline of 0.9%. This decline brings some welcomed relief in costs for some materials and services. On the goods front, prices for final demand goods remained unchanged in June, following a decline of 1.6 % in May. The graph below illustrates the year-over-year percent change in a composite index of construction materials, represented by the red line. We observe a noticeable upturn in this trend, which raises concerns as it typically precedes bid price changes (blue line) by approximately 12 months. If this upturn persists, it could potentially lead to an increase in bid prices in 2024, which might pose challenges for the construction industry. It is worth noting that certain sectors, such as the lumber industry, have continued to experience disinflationary trends. This is particularly promising for the residential sector, which heavily relies on lumber, creating an optimistic outlook for the housing market’s anticipated growth in the upcoming year. However, the index for final demand energy showed a noteworthy increase of 0.7%. This indicates potential cost increases in the production of certain materials, like cement (13.3%) and concrete (11.3%), which have continued to rise.

In summary, the June PPI release reveals a slight increase in final demand prices, primarily influenced by services excluding trade, transportation, and warehousing. This finding aligns with expectations of another Federal Reserve rate hike at their upcoming July meeting. The construction industry, facing ongoing challenges, will continue to grapple with the persistent upward trend in prices and the impact of inflation. While there are signs of improvement, inflation remains a stubborn issue that requires careful management and strategic approaches from the Fed.