By Ralph Flores, Economist at Dodge Construction Network

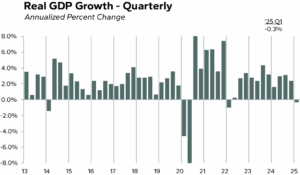

While some sectors like institutional and infrastructure remain stable, overall construction activity is likely to come under pressure as commercial and residential building face mounting challenges. The Bureau of Economic Analysis (BEA) has released its advance estimate for the first quarter of 2025, revealing that real gross domestic product (GDP) decreased at an annual rate of 0.3%. This marks the first contraction in GDP since early 2022 and a notable reversal from the 2.4% growth recorded in the fourth quarter of 2024.

Importantly, the bulk of the decline was due to a sharp surge in imports, especially consumer and capital goods, which are subtracted in GDP calculations. Imports rose at an annualized rate of 41.3%, subtracting 5% from growth, as businesses rushed to place orders ahead of expected tariffs. Excluding this surge in imports, the domestic economy continued to expand. A decrease in government spending, particularly federal defense expenditures, also weighed on growth, though this was partially offset by gains in private investment, consumer spending, and exports.

Consumer spending growth moderated under the weight of persistent inflation, with gains in services—especially health care and housing/utilities—and nondurable goods partially offset by a decline in durable goods purchases. This mix of strength and weakness adds complexity to the economic picture, raising concerns about stagflation risks. Still, there are signs of resilience: real final sales to private domestic purchasers rose by 3.0%, a slight uptick from the prior quarter, indicating underlying demand remains firm. At the same time, inflationary pressures accelerated, with the gross domestic purchases price index jumping to 3.4% from 2.2% in Q4, and the PCE price index climbing to 3.6% (3.5% core). These figures highlight the delicate balance the Federal Reserve is trying to strike, curbing inflation without derailing growth, as it navigates toward a soft landing.

For the construction industry, the GDP decline may cause confusion, but doesn’t signal a pullback in actual activity. Public construction and select nonresidential sectors like healthcare remain supported by steady investment and underlying demand. On the residential side, housing activity—the largest construction sector—showed resilience in the first quarter, with residential fixed investment contributing positively to GDP. However, looking ahead, residential construction faces significant headwinds as high interest rates, tighter credit conditions, and consumer uncertainty threaten to dampen future demand.

Even though the economy is not in recession, the psychological impact of a negative GDP print could continue to affect consumer sentiment and business confidence, further stalling decision-making for large investments, including construction. As such, even without a material shift in fundamentals, perception may matter more than the data suggests. Looking ahead, the focus will remain on inflation trends, import normalization, and the Fed’s response, while staying alert to how tariffs reshape supply chains and contractor pricing strategies. For construction, balancing actual demand with sentiment requires vigilance toward trade policy shifts, as escalating tariffs may force developers to reassess budgets and sourcing plans.