by Olevia Sharbaugh Starkey, Economist at Dodge Construction Network

The effects of a recession on the construction industry are numerous. Reduced demand for costly construction projects, more expensive and drawn-out project timelines, and tighter access to financing can combine to make construction-related companies feel the pressure from all sides. Commercial projects, such as those in the office, hotel, and retail sectors, are often the hardest hit as they are the least insulated from shifting market dynamics. However, recessions can sometimes create opportunities—if you know where to look.

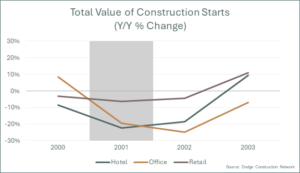

The early 2000s recession, characterized by the collapse of the inflated technology stock market, hit the U.S. in March of 2001 and lasted until November of that year. Though the “dot-com bubble,” as it has been termed, had little to do with the construction industry, the effects of this downturn were vast. From 2000 to 2001, the total value of construction starts in the hotel sector fell 22%, office construction fell 19%, and retail stores fell 6%. Companies were unwilling or unable to secure financing for new buildings in these commercial sectors. Therefore, construction starts in this period fell.

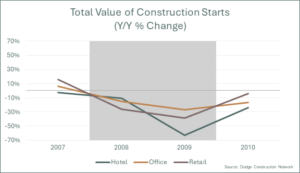

After the Global Financial Crisis (GFC) began in late 2007 and extended into 2008 and 2009, key commercial construction sectors began to feel devastating effects similar to those of the early 2000s recession. The total value of retail construction starts dropped 55% from 2007 to 2009. Office construction was not far behind, falling 38% in the same time period, and new hotel construction declines were the most pronounced, falling 67%. This recession was triggered by a combination of factors, including the collapse of the housing bubble, risky lending practices, and the failure of major financial institutions, particularly those involved in the mortgage and banking sectors. Given that the single-family housing market is a driver of growth among many other construction sectors, it is no surprise that its collapse, combined with more restrictive lending standards from banks, led to a decline in the construction of hotels, office buildings, and retail stores.

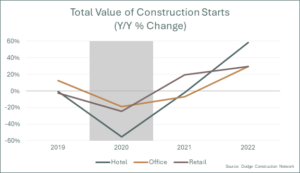

Although the recession that occurred in 2020 following the COVID-19 pandemic was not as prolonged as the recessions mentioned above, Dodge Construction Network saw a similar trend in construction value movement. From 2019 to 2020, the total value of hotel starts declined 55%, retail construction dropped 24%, and office construction fell 19%.

These commercial categories were significantly impacted by the recessions mentioned above, experiencing both direct and indirect consequences from each of them. Financial instability, declines in demand for commercial construction, and project delays are all commonplace during recessionary periods and can lead to tough times for construction companies. However, there may be a caveat to this negativity. Dodge Construction Network tracks two different series that capture the total value of construction starts: new and additions value and alterations value. While the new and additions value of construction declines considerably during a recession, as is expected, alterations (or renovations) may provide an avenue for growth and lessen the strain construction-related companies typically face in an economic downturn.

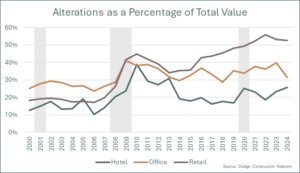

Alterations as a percentage of the total value of construction starts in these commercial categories clearly illustrate how recessions impact renovations. As shown in the figure below, the share of alterations increased in all three categories during the early 2000s recession and the GFC. It remained elevated a year after before returning to more normal levels. This rise can be attributed to more significant declines in the new and additions value of construction compared to alterations value during a recession, resulting in alterations becoming a larger portion of the construction market in these commercial sectors.

With the exception of the office sector, all categories also experienced an uptick in alterations share in 2020. The slight decline of the alterations share in the office sector could be due to a combination of two factors: the historically elevated alterations share in 2019 and the nature of the Covid-19 recession. Office alterations as a share of total value of construction starts in 2019 were already at a slightly elevated level of 35%, four percentage points higher than the average from 2000 to 2018 at 31%. This elevated level made a decline in 2020 much more likely as the market corrected. However, it was still three percentage points higher than the average at 34%. Additionally, the nature of the Covid-19 recession and the beginning of the work from home culture could also have motivated a pause for any planned office alterations as the sector began to grapple with a new normal.

Examining more recent history, this post-pandemic period appears a bit unique compared to the other post-recessionary periods. For example, 2021 through 2023 also experienced rises in the alterations in the share of total value for the retail and office sectors. In contrast, the years following the early 2000s recession and the GFC saw a moderation in share.

The retail sector’s alterations share has been rising since 2015 and is currently significantly higher than historical levels at around 53% in 2024. The rise in e-commerce and the subsequent lack of demand for new and costly brick-and-mortar retail stores is likely a primary driving force behind this trend. For example, large retailers such as Walmart and Target have mainly focused on renovations for the past few years, likely due to these underlying trends (Walmart and Target account for the bulk of alterations in the retail sector).

The office sector’s alterations share has also been performing well since the pandemic, a byproduct of the general lack of demand for new office space as many companies have switched from fully in-person work to a hybrid or remote work environment. The one section of the market that remains moderately healthy, however, is the luxury office sector. As the demand shifts toward high-quality office space, office renovations are taking place to meet this need with more modern and up-to-date buildings. Dodge Construction Network tracks both data center and traditional office construction under the office category. When examining only the traditional office sector (without data centers), the elevated alterations share of construction value becomes even more apparent, averaging over 50% from 2022 to 2024. This indicates that alterations have become the majority of the traditional office market, a stark change from before the COVID-19 pandemic, when they averaged 24% (from 2000-2019).

The hotel sector, which increased the most during the COVID-19 recession, saw a slight decline in alterations share in 2021 and a sharper decline in 2022 before returning to growth in 2023 and 2024. However, the larger decline in 2022 was entirely due to an outsized increase in the new and additions value of construction starts for the hotel sector, not a decline in the value of alterations starts, as those increased 28% over the year. This recent increase in alterations share for the hotel sector is likely due to a new trend among top hotel brands such as Marriot International, IHG, and many others. These companies are focusing their expansion efforts on renovations of existing hotels as a faster and more affordable alternative to new construction. As travel demand in the form of “revenge travel” has increased substantially since the end of the mandated quarantines of 2020-2021, speed to market to meet this demand has become a crucial element in the hotel industry’s strategic planning.

Alterations typically rise as a share of total construction value during a recessionary period due to increased caution among investors. A brand-new office building or hotel is much more expensive, time-consuming, and risky than one that already exists, but needs a makeover. In a market that is experiencing volatility and uncertainty in the future, ways to mitigate risk while still investing in what is to come are likely much more appealing to the average business.

Recognizing that office, retail, and hotel construction shifts toward renovations during a recession is crucial for adjusting business strategies. By understanding market dynamics such as tighter budgets and the focus on existing infrastructure, companies can better position themselves to meet the demands of a renovation-focused market, potentially creating new opportunities in a time when very few exist. While not a guarantee, simple changes such as emphasizing renovation services in marketing materials during an economic downturn could mean the difference between staying afloat or sinking. Additionally, total commercial alterations have continued to increase in value since the end of the COVID-19 recession in 2021, indicating that this portion of the construction market remains healthy. As we enter 2025 and economic uncertainty increases, alterations are likely to continue performing well and should be accounted for in near-term business strategies.