By Lilli Tillman Smith, Industry Analyst, and Eric Gaus, Chief Economist

Why the Gap Looks Closer to 1.2 Million Units and What It Means for Construction and Building Materials

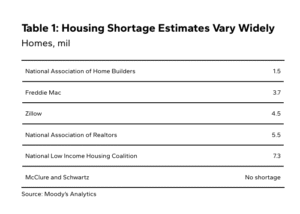

The narrative of a severe U.S. housing shortage has dominated industry commentary for years. Escalating housing costs represent the most apparent first sign of underlying issues, but estimates of the underlying shortage vary widely (Table 1). Methodological choices explain most of this divergence. Dodge Construction Network’s analysis indicates the shortage peaked around mid‑2022 at roughly 2 to 3 million units and has since narrowed to approximately 1 to 1.5 million units.

Why the Shortage Is Closer to One Million Units

Our approach relies on vacancy rates because vacancy reflects only units that are truly available for occupancy, avoiding distortions from seasonal or off market homes. When vacancy falls below its equilibrium level, rents and prices rise faster than incomes. If the United States were short by several million units, vacancy rates would be falling sharply. Instead, they are stabilizing.

Rental vacancy reached 7.2 percent in Q4 2025, showing that the large 2024–2025 multifamily delivery wave is finally loosening the rental market. Homeowner vacancy stayed at 1.2 percent, still low but no longer tightening, indicating stabilization rather than further scarcity. Multifamily vacancies continue to rise and rents have fallen more than six percent from their 2022 peak, confirming clear easing in private rental conditions. During 2020–2022 shortages were measured in millions, but by 2024 the estimated gap had narrowed to 3.8 million, with 2024–2025 supply growth bringing remaining deficits closer to tens of thousands rather than millions.

Household formation fell sharply during the pandemic and remained soft because affordability constrained moves. Some argue that this created pent-up demand not yet visible in the data. The conclusion is that the shortage is real but much smaller than the multimillion unit claims often used to justify aggressive long-term construction forecasts.

Why the Market Could Approach Balance by 2027 or 2028

Three structural factors point toward equilibrium within a few years.

1. New Construction Will Remain Solid but Not Accelerating

Multifamily completions reached multi‑decade highs in 2024 and 2025. This is documented in Dodge Construction Network’s construction starts and completions data, which shows total residential units declining modestly in 2025 but stabilizing in 2026 at over 1.5 million units, adding further to available stock.

2. Household Formation Is Slowing

Household formation peaked in the mid‑2020s and is now decelerating. Dodge baselines show formation falling from about 1.2 million in 2025 to roughly 860,000 in 2026 and about 615,000 by 2028. Slower population growth, demographic aging, and recent immigration trends reinforce this slowdown. This matters because demand pressure weakens when population and household growth slows.

3. Housing Starts Are Expected to Remain Steady

Dodge expects U.S. housing starts to average 1.5 to 1.6 million units per year through the decade. When set against expected formation and normal demolition, this pace gradually closes the remaining gap rather than widening it.

Combined, these forces suggest that by 2027 or 2028, new construction will only need to keep pace with ongoing demand.

Why Shortage Relief Does Not Guarantee Affordability

A shrinking shortage does not eliminate affordability problems. Harvard’s State of the Nation’s Housing report shows renter cost burdens at record levels in 2025. Vacancies are rising, yet insurance, taxes, interest rates, and construction costs remain elevated. New supply has tilted toward higher-amenity, higher-rent multifamily units, while entry-level construction remains constrained by zoning and land availability. The affordability challenge today stems more from a mismatch between incomes and available units than from extreme physical scarcity.

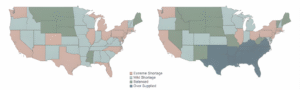

A Fragmented Housing Market: Vacancies Diverge by Region

National averages obscure significant geographic divergence.

Housing Shortage by State Q2 2022 vs Q4 2025

Regional variation is significant. The Sunbelt has built well ahead of demand, much of the Midwest is close to balanced, and the Northeast and West Coast remain structurally tight due to regulatory constraints. These differences will continue to shape construction activity by requiring manufacturers and builders to rely on regional demand signals rather than a single national narrative.

Implications for Building Products and Construction

1. New Construction Will Remain Solid but Not Accelerating

Residential starts remain near 1.5 million units in 2025 and are expected to settle around 1.4 million annually by 2030. This supports steady structural materials demand but does not indicate a super cycle.

2. Multifamily Materials Demand Has Likely Peaked

Record multifamily vacancy and cooling starts imply softening demand for materials tied to large multifamily projects by 2027.

3. Remodeling Should Strengthen as Mobility Improves

Mortgage lock in has depressed mobility and suppressed remodeling activity. As rates ease, turnover driven renovations will increase, benefiting roofing, insulation, HVAC, and building envelope categories.

4. Unit Size and Type Are Shifting

Dodge data indicates that median new home sizes continue to decline. Smaller units reduce structural volume per home but may increase demand for some product categories; roof area ratios may improve, and new construction may support more volume of insulation driven by code requirements.

5. Regional Variation Is Now a Primary Driver

Demand will cool in high vacancy Sunbelt markets and remain steady or strong in the Northeast, Midwest, California, and Washington.

6. A Smaller Shortage Requires Strategic Recalibration

If the true gap is nearer 1.2 million units, long term growth will depend more on:

- Renovation and replacement

- Energy efficiency upgrades

- Turnover driven projects

- Targeted construction in constrained regions

Manufacturers and distributors should prepare for a stable, sustainable market rather than expecting capacity expansion tied to claims of a multimillion unit deficit.

Conclusion

The United States faces real housing challenges, but vacancy data, demographic patterns, and construction activity indicate a narrowing supply gap. Dodge Construction Network data points to moderating demand and substantial new supply that is moving the market toward balance. The decade ahead will be shaped less by catching up to a large deficit and more by adapting to a stable but fragmented market defined by demographics, affordability pressures, and regional variation.

Want more perspectives like this? Follow Lilli Tillman Smith and Eric Gaus on LinkedIn for ongoing commentary on the forces shaping construction.

Related Articles:

2025 vs 2024 Top Commercial and Multifamily Construction Starts

January Update on Census Housing Starts and Construction Put-in-Place Spending